Key Takeaways

Opening a business bank account in the UAE is a structured process where clarity, consistency, and preparation determine both speed and approval outcomes.

Banks assess risk, not just documentation, so alignment between business activity, structure, and financial profile is essential.

Complete and consistent documentation reduces delays, particularly during KYC and compliance checks.

Choosing the right bank and preparing early improves approval timelines and avoids unnecessary rework.

Establishing a company in the UAE involves more than registration. It requires a financial setup that supports how the business will operate. Opening a business bank account is a key part of that process, yet many applications stall despite complete documentation. Delays and rejections rarely come down to missing paperwork. They stem from how the business is assessed during review. Approaching the process with that understanding reduces friction and shortens the path to approval.

Why Business Bank Account Approval in the UAE Is Complex

Banks in the UAE operate under strict compliance requirements. Every application is reviewed through KYC (Know Your Customer) and AML (Anti-Money Laundering) checks, where the focus is on risk, not just documentation.

Approval depends on how the business is assessed during review. Clear activity, a consistent structure, and aligned documentation move faster through the process. Where the licence, business plan, and transaction profile do not align, delays follow.

Most applications stall due to unclear business activity, inconsistent documents, or an incomplete explanation of the source of funds. Addressing these areas early reduces friction and improves the likelihood of approval.

What Banks Evaluate Before Approving a Business Bank Account

Before an account is approved, banks assess how the business operates, who is behind it, and how funds will move through the account.

Business Activity and Risk Profile

Banks categorise businesses by risk level based on activity and exposure. Trading companies, cross-border consultancies, and businesses operating in high-risk sectors or regions are subject to closer review. A clearly defined activity makes the assessment more straightforward.

Company Structure and Jurisdiction

The legal structure of the company affects both eligibility and conditions. Understanding how mainland and free zone setups differ is essential for banking access. Free zone companies are widely accepted but may face restrictions depending on the zone and activity. Offshore entities have more limited options and require more detailed documentation.

Ownership and Source of Funds

Banks review all shareholders and authorised signatories. This includes financial history, professional background, and country of residence. A clear explanation of how the business is funded helps reduce delays during compliance checks.

Expected Transaction Activity

The bank also reviews how the account will be used. This includes transaction volume, currencies, and the location of clients or suppliers. Inconsistent or unclear information at this stage often leads to additional queries or delays.

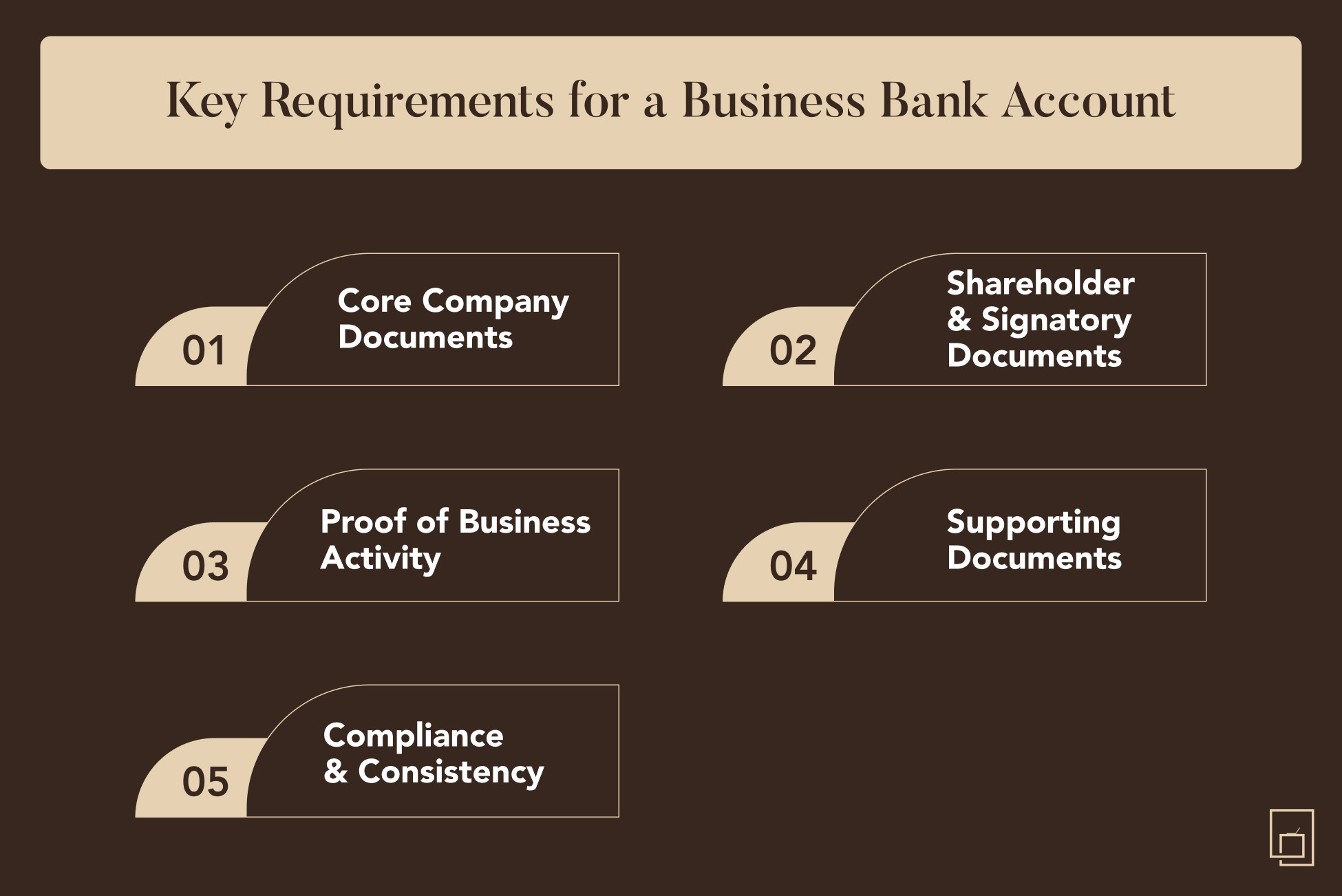

Key Requirements to Open a Business Bank Account

Banks expect a complete set of documents that clearly reflect how the business is structured and how it will operate.

Core Company Documents

A valid trade licence, certificate of incorporation, and Memorandum and Articles of Association are required by all banks. These must be current and aligned with the stated business activity.

Shareholder and Signatory Documents

Passport copies for all shareholders and authorised signatories are required. UAE residents must provide a valid visa and Emirates ID. Most banks also request personal bank statements covering the past three to six months.

Proof of Business Activity

Banks require evidence that the business can demonstrate real or planned activity. This may include signed contracts, invoices, letters of intent, or existing trading records. Applications without clear activity often face delays.

Supporting Documents

A business plan or company profile, a source of funds declaration, and bank reference letters can strengthen an application. While not always listed as mandatory, they help address compliance checks.

Ensuring documents are correctly prepared and attested often requires coordination with local authorities, a process typically handled through PRO services.

Consistency across all documents is critical. Where the trade licence, business profile, and supporting records do not align, banks will raise questions.

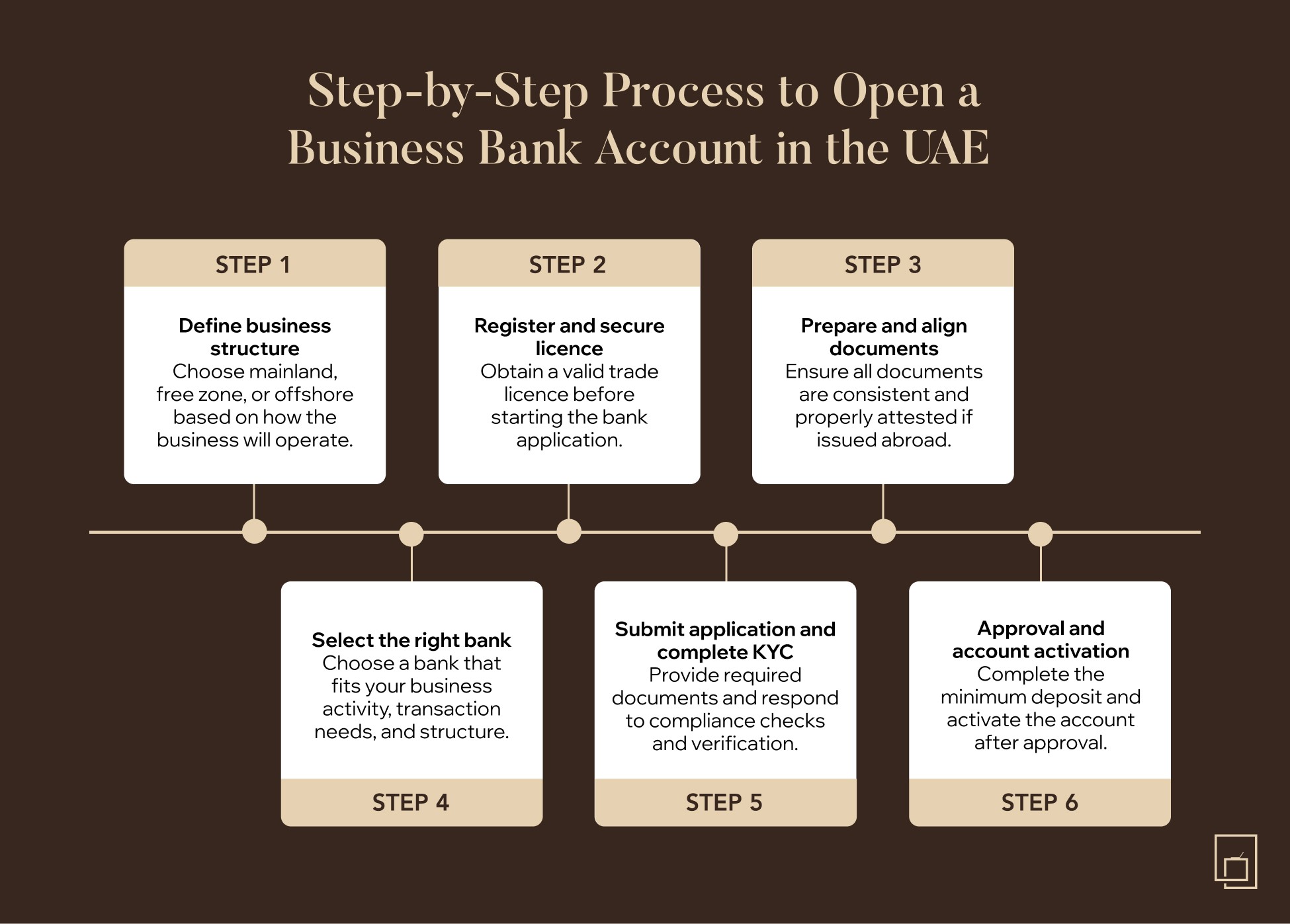

Step-by-Step Process to Open a Business Bank Account in the UAE

Opening a business bank account follows a structured sequence. Delays usually occur when one of these steps is incomplete or misaligned.

Step 1: Define Your Business Structure

Decide whether the company will be established on the mainland, in a free zone, or as an offshore entity. This choice affects banking access, documentation requirements, and approval timelines.

Step 2: Register Your Business and Secure a Licence

A valid trade licence is required before any bank application can proceed. Businesses still in the formation stage often benefit from structured support through business setup services in the UAE.

Step 3: Prepare and Align Documentation

Gather all required documents and review them for consistency. Documents issued outside the UAE may require notarisation, consular attestation, and authentication through the UAE Ministry of Foreign Affairs. This process can take one to two weeks, depending on the country of origin.

Step 4: Select the Right Bank

Bank selection should reflect how the business operates. Local banks are often suited to UAE-based activity, while international banks may be more appropriate for cross-border operations.

Evaluate:

Fees and minimum balance requirements

Industry acceptance

Digital banking capabilities

Step 5: Submit the Application and Complete KYC

Once submitted, the bank begins its compliance review, which may include additional document requests, interviews with a relationship manager, and verification of business activity. Delays at this stage are usually linked to incomplete or unclear information.

Step 6: Approval, Deposit, and Activation

After approval, the bank confirms the required minimum deposit. Once the account is funded, it becomes operational for transactions and day-to-day use.

Business Bank Account Options in the UAE

Banks in the UAE offer different account types depending on how a business operates and manages its finances.

Current accounts: used for day-to-day operations, including supplier payments and client receipts. Most businesses start here due to ease of access and transaction flexibility.

Savings accounts: suited to holding surplus funds and earning interest, with more limited transaction use.

SME and corporate accounts: structured for growing or established businesses, often with features such as trade finance, payroll support, and dedicated relationship management.

Multi-currency accounts: designed for businesses that operate across borders, allowing transactions in multiple currencies while reducing conversion costs.

Digital Banking and Fintech Alternatives

Digital banking platforms offer a faster entry point, particularly during early setup, particularly during early setup. They often require lower balances and support multi-currency transactions, which can be useful for cross-border activity.

However, they do not replace a traditional business bank account. Many are not accepted for regulatory processes such as visa applications or government transactions. For most businesses, digital platforms support specific operational needs, while a corporate bank account remains central to how the business functions.

Opening a Business Bank Account for UAE Residents

The application process is generally more straightforward for individuals with an established presence in the country. A valid Emirates ID and local address simplify identity checks and reduce some verification steps for UAE residents.

Residency improves access, but it does not guarantee approval. Banks apply the same compliance standards to every application. Where business activity is unclear or documentation is inconsistent, delays still occur.

Opening a Business Bank Account for Non-Residents

Additional verification is required where there is no established presence in the UAE. Foreign-issued documents must be certified by the relevant UAE consulate and attested by the UAE Ministry of Foreign Affairs. Some banks also require in-person verification, which may involve travelling to the UAE.

Approval timelines are typically longer, often ranging from two to four weeks or more depending on the business structure. Higher minimum balances are common, and fewer banks accept non-resident or offshore applications. Choosing a bank with experience in international clients, and reviewing fees, transfer costs, and digital access in advance, helps reduce delays and avoid unnecessary rejections.

Fees, Charges, and Minimum Balance Requirements

Costs vary significantly between banks, and understanding how they are structured helps avoid unexpected expenses over time.

Common Banking Fees

A business bank account typically includes several recurring and transactional costs:

Monthly maintenance fees for account upkeep

Transaction charges for transfers, deposits, and withdrawals

International transfer fees for cross-border payments

Foreign exchange markups on currency conversions

These charges differ by bank and account type, particularly between SME and corporate accounts.

Minimum Balance Requirements

Banks require a minimum balance to be maintained at all times. The required amount varies depending on the account type and bank.

Falling below this threshold usually results in monthly penalties. Over time, these charges can reduce working capital, particularly for businesses with fluctuating cash flow.

How to Evaluate the True Cost

Headline fees do not reflect the full financial impact of maintaining an account. For businesses operating across borders, currency conversion markups and international transfer charges often exceed standard monthly fees.

Before opening an account, review the full fee schedule, including:

Foreign exchange margins

Wire transfer costs

Penalties linked to minimum balance requirements

This provides a more accurate view of long-term banking costs.

How Long It Takes to Open a Business Bank Account

For a well-prepared and aligned documentation, the process typically takes two to four weeks. Applications involving non-residents, complex ownership structures, or higher-risk activities take longer.

Delays are most often caused by incomplete or inconsistent submissions. When documentation is aligned from the outset, timelines become more predictable.

Common Challenges and How to Improve Approval Outcomes

Incomplete or inconsistent documentation is the most common cause of application failure or delay. Applications also stall when banks cannot clearly understand the business activity, ownership structure, or source of funds.

High-risk industries, unclear transaction activity, and weak financial transparency lead to stricter review. Most rejections are not based on eligibility, but on how the business is presented during assessment.

Improving outcomes depends on clarity and alignment. The trade licence, business plan, and transaction profile must reflect the same activity. A clear explanation of clients, revenue sources, and expected transactions, supported by financial history or projections where available, reduces delays and strengthens the application.

How Business Setup in the UAE Influences Banking Approval

Banking outcomes are closely tied to how the company is organised. A business with clearly defined activity, a compliant legal structure, and consistent documentation is easier for a bank to assess and approve.

Where the structure does not reflect actual operations, or introduces unnecessary complexity, additional compliance checks follow. This often leads to delays or rejection.

Professional support becomes valuable where ownership is complex, shareholders are based in multiple jurisdictions, or the business is entering the market for the first time. Structuring the company correctly from the outset reduces risk and improves the likelihood of approval.

A registered office address also strengthens credibility. Even where a physical office is not required, a compliant business address, such as a virtual office, demonstrates a clear operational presence.

Preparing for Business Bank Account Approval

Banking outcomes depend on preparation and clarity. Every document, statement, and response during the KYC process should present a clear and consistent view of the business.

Companies that structure correctly before approaching a bank move through the process with fewer delays. When banking is treated as an afterthought, issues often surface later in the form of additional checks or rejected applications.

Frequently Asked Questions

How do you choose the right bank for a business account in the UAE?

Can an account be opened before the company starts generating revenue?

Can a business bank account be opened remotely?

Is it allowed to use a personal bank account for business transactions?

Can a company hold more than one account in the UAE?